For decades, companies of all shapes and sizes and operating in all sectors regularly engage in the practice of leasing assets.

For businesses, leases have various benefits, including increased purchasing power, optimized upkeep costs, and improved cash flow management.

A company that rents out its assets or takes out leases from third parties must monitor the effect this has on its bottom line. Aside from being required by law, this practice, known as lease accounting, can aid in the smooth operation of a business.

So, in this extensive guide on lease accounting, we discuss what it is, its implications, and the key differences between lease accounting under old vs. new standards. Let's dig deeper.

The term "lease accounting" is the process through which a business keeps track of the financial implications of the leasing endeavors.

Financial statements (balance sheet, cash flow statement, and income statement) must include information on leases that are classified in a certain way.

Each party associated with a lease (whether a lessee or a lessor) has a different accounting treatment of lease transactions on its financial statements.

When kept in order, these three recordings provide an accurate depiction of a business's asset value and the lease's influence on the business's bottom line.

A company's leases must be categorized as either "operating" or "financing," depending on the lease duration, to report them accurately in financial statements.

Furthermore, pronouncements made in the last several years have caused significant shifts in this accounting arena.

Since the new lease accounting standards have become mandatory, all leases, including operating leases, must be recorded on the balance sheet. Earlier, only capital and finance leases were required to be recorded there.

There are many different aspects of lease accounting to think about, and each plays a significant role in delivering financial insights that can affect organizational planning and drive decisions, which is why accounting is so important.

It's an instrument that allows access to vital data, yields insightful conclusions, broadens one's perspectives, and facilitates better judgment calls.

Knowing how a lease should be classified and being up-to-date on the latest lease accounting standards are both crucial.

As a result, professionals need to understand the role of lease accounting for all financial statements to make well-informed judgments and formulate effective plans.

How a company documents the assets, liabilities, earnings, and expenditures from leasing activities can affect the broader sense of its finances and, by extension, its business strategy, whether the business acts as the lessee or the lessor.

When referring to the various parties engaged in a lease arrangement, the terms "lessor" and "lessee" are the most common to employ.

This differentiation is crucial since the accounting for a leased asset done by a lessor is vastly distinct from the accounting done by a lessee.

The fundamental definitions of the terms "lessor" and "lessee" did not shift while new lease accounting standards were released by the numerous accounting boards that serve local, foreign, and government-related organizations.

However, the new lease standards did call for some modifications to the accounting treatment that lessors and lessees are subjected to.

The entity responsible for making payments to a lessor in exchange for permission to use a specified asset or property is known as a lessee.

For instance, a person who leases an automobile from a dealership is considered the lessee because they are the one using the vehicle. The lessee is essentially making a payment to the lessor for the "right to use" the asset in question.

Lessees are now required by the latest lease standards to record an intangible ROU asset or a lease asset in their books when they enter into a lease.

It's important to note that this asset gets recorded on the lessee's accounts as an intangible asset instead of a fixed asset.

Based on criteria laid out in the standards, lessees can determine whether a given lease is an operating or a finance lease. Accounting treatment for the two forms of leases is a bit different -

A person, firm, or organization that grants another party the authorization to utilize an asset for a predetermined period in exchange for payment is known as a lessor.

When two parties enter into a lease contract, one party often rents the property it owns to the other party in return for a monthly payment. It is one of the most typical lease agreement cases.

If a company, for instance, owns a property and leases the right to use the facility or space within the property, the entity that owns the building is the lessor, which is also a popular term for the landlord.

Based on the criteria outlined in the standards, lessors will categorize leases as sales-type, direct financing, or operating.

In the case where a lease is very similar to selling an asset, the lessor's initial accounting will look quite similar to that of a sale.

The traditional lease accounting standards consisted of ASC 840, IAS 17, and several other GASB standards, most notably GASB 13 and GASB 62.

Prior to the publication of the new lease accounting standards, many businesses did not consider it important to pay special regard to operating leases inside the context of the financial reporting procedure.

The reason is that operating leases only entail an expense for the lessee throughout the lease duration and have minimal implications on the lessee's balance sheet.

Since the previous standards mandated that capital leases get recognized on the balance sheet, accounting for these types of leases was one of the most complicated aspects of leasing under the previous guidelines.

IAS 17 refers to these types of leases as finance leases. On the financial accounts, both the capitalized liabilities and assets associated with capital/finance leases were reported and then amortized over a predetermined amount of time.

The off-balance-sheet approach of operating leases is something the new lease accounting standards aim to put an end to.

Including operating leases in the balance sheet clarifies a business's financial liabilities and the assets necessary for business operations, improving the understandability of financial statements.

Lessees, particularly those with operating leases, must pay for the advantage of transparency. Lessees must start adjusting to the new standards by compiling a comprehensive list of their running leases, which can be a significant amount of paperwork.

Then, they have to perform a plethora of accounting computations, many of which are quite involved. Capital leases, which are now known as finance leases, experienced fewer regulation changes. As a whole, lessor requirements were quite consistent.

To account for these shifts in the lease, new guidelines have been established, including:

The Financial Accounting Standards Board (FASB), the organization responsible for establishing US GAAP, has issued this standard.

According to ASC 842, there are three types of lessor leases- sales, financing, and operating and two types of lessee leases - financing and operating. This dual accounting treatment is also mandated by this document.

ASC 842's objective is to improve financial reporting for leases that are just leases transformed into purchases. This regulation first took effect for publicly traded corporations in 2019 and for privately held businesses on December 15, 2021.

Let's consider an example.

In order to standardize worldwide financial reporting, the IASB published IFRS 16. It prescribes a uniform method of accounting for all leases, similar to ASC 842's approach to financing leases.

Companies based in the United States with overseas parents or subsidiaries should be familiar with IFRS 16, and the differences between it and the US generally accepted accounting principles (GAAP). On January 1, 2019, this regulation went into force.

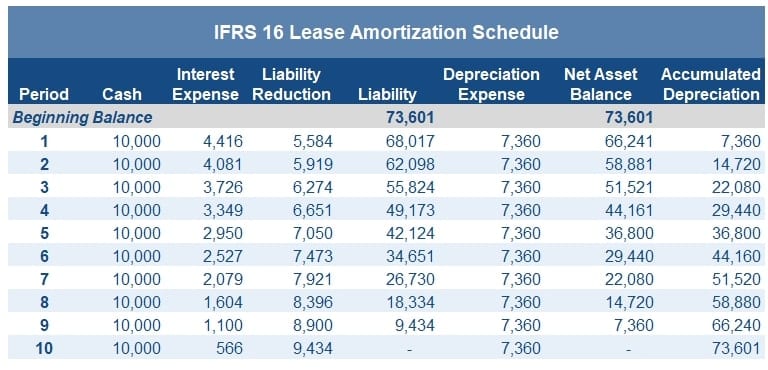

Consider the below example to get a brief idea about lease accounting under IFRS 16.

The following procedures will be used to produce the IFRS 16 amortization schedule based on the foregoing facts.

The amortization schedule as of the lease's commencement is as follows.

The GASB is comparable to the FASB, but it sets generally accepted accounting principles (GAAP) for local and state governments.

By adopting a uniform method of accounting for leases similar to that of IFRS 16, GASB 87 modernized lease accounting guidelines for its members.

At the lease commencement date, government agencies that are required to report under GASB 87 are required to record both a lease liability and an associated lease asset.

The present value of the anticipated lease payments made during the period of the lease is equivalent to the lease liability, and the accompanying lease asset is equivalent to the lease liability with a few small changes made to it. GASB 87 went into effect on June 15, 2021.

GASB 87, just like IFRS 16, employs a single modeling framework in which all leases are categorized as finance leases.

The new standard introduces a substantial change in that it requires the recognition of a lease liability and a lease asset for all leases that were previously categorized as operating.

Following GASB 87, lessors must initially recognize both lease receivables and a deferred inflow of resources when the lease period first begins.

A lessee's lease receivable is determined in the same way as the lessee's lease liability: it is equal to the current value of the lease receipts that are anticipated to be received over the lease duration.

The deferred inflow of resources is comparable to deferred revenue in that it is equivalent to the lease receivable after a few small changes have been made to the calculation.

Under this standard, the GASB had the intention of having the accounting for lessors effectively parallel the accounting for lessees.

It is achieved when both the lessee and the lessor each recognize the present value of the projected remaining lease payments, respectively, and then offset that value with the matching ROU asset and the deferred resources inflow.

Let's take an example with the following details:

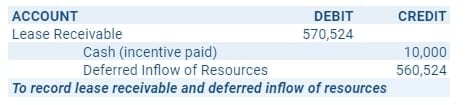

With a discount rate of 2% applied to the outstanding lease payments from the start of the lease, the present value of those payments equals $570,524.

Here, the lessor rewarded the lessee with an incentive at the outset of the lease. Therefore, the deferred resources inflow at the start of the lease is determined by subtracting the incentive payment of $10,000 from the lease receivable total.

The deferred inflow of resources is determined to be $560,524 after accounting for the incentive payable to the lessee.

Examining the commencement of lease journal entry, we have $570,524 lease receivable debited, the $560,524 deferred inflow of resources credited, and the $10,000 commencement incentive provided to the lessee gets credited. It then follows subsequent journal entries.

For the most part, the definitions and other terminology used for different types of leases are consistent across the three new lease accounting standards.

While IFRS 16 and GASB 87 both employ a standardized format for accounting, ASC 842 uses a dual approach.

Enlist a professional lease accountant to guide other discrepancies, such as how to include lease payments in the statement of cash flows, when to reprice a lease to compensate for a change in lease terms or deficits, and whether or not any prior fiscal periods should be reiterated in the financial statements being compared.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}