Sign In

Get a Demo

.jpg)

With every major accounting standard released by the Governmental Accounting Standards Board (GASB), organizations find it challenging to comply with and keep track of the leases.

The GASB released statement no. 87 in June 2017. In an effort to make financial information more actionable, the GASB has mandated that all leases with terms longer than a year be represented as liabilities and right-of-use (ROU) assets.

This extensive guide on GASB 87 covers all crucial aspects of this lease accounting standard. So, let's dig deeper.

GASB 87 is the most up-to-date standard for lease accounting and financial reporting established by the Governmental Accounting Standards Board (GASB).

GASB 87 is applicable to local and state governments, and it will coexist with two additional new lease accounting standards for leases: ASC 842 and IFRS 16.

The main purpose of GASB is to provide residents, lawmakers, government bond analysts, and other stakeholders with data and information that will assist them in the decision-making practice for decisions pertaining to governmental institutions.

So, unless anything is mentioned, all state and local governmental bodies, such as airports, public welfare organizations, public employee pension systems, utility services, healthcare facilities, schools and universities, and so on, are required to comply with its declarations.

The Board's primary motivation for kicking off the standard was the need to ensure that all leases would be accounted for in the same manner.

When this is done, leases are classed on accountancy sheets as financing sources of the ROU asset for a specified amount of time. This classification is more precise than the previous ones.

Rather than preserving the former differentiation between operating and capital leases, GASB 87 leases are now commonly labeled financings.

Organizations need to comprehend two aspects to fully conform to the standards of this latest statement. First, they need to recognize whether or not GASB 87 impacts books from past years, and second, they need to comprehend the requirements for recognizing GASB 87 leases.

Some of the critical steps involved in the GASB 87 standard are as follows:

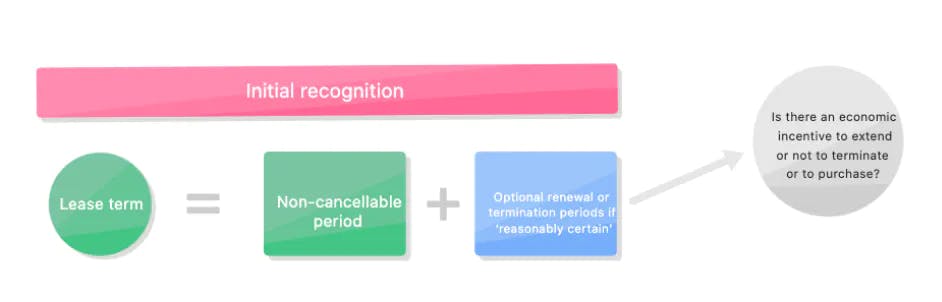

This refers to the current value of the prospective lease payments that must be paid throughout the lease duration.

The asset value represents the sum of the initial assessment of lease liabilities plus any additional payments made by the lessee over the period of the lease's term, minus any lease incentives obtained from the lessor.

The establishment of an asset and a liability on the financial position statement results from the recording of an initial journal entry for GASB 87 leases.

Over the course of the lease term, the asset representing the right-of-use gets written off, also known as amortized, and recorded as a resource outflow.

This is intended to act in a manner analogous to a depreciation expense, reflective of the gradual decline in the value of an asset with time.

The lease liability will be reduced over time as a result of successive journal entries, and the interest expenditure associated with the leased asset will be recorded.

The interest rate gets multiplied by the outstanding liabilities balance after the previous period to determine the latter.

The ultimate objectives of GASB 87 are:

1. Enhance the relevance of governments' financial statements by mandating the declaration of specific lease liabilities which are not now required to be reported.

All leases need to be declared in accordance with GASB 87 as either a capital or a finance lease.

This eradicates the categorization of an operating lease unless such a lease is considered a short-term lease, which is defined as a lease for a length of 12 months or lesser.

2. Lessees and lessors should be required to record leases using a unified framework so that the financial accounts of government entities can be compared more easily with one another.

According to GASB 87, there are three different accounting treatments, and they are as follows:

Further, a lessor is accountable for recording a lease receivable and a deferred resources inflow in accordance with GASB 87.

A lessee must recognize a lease liability and an intangible ROU lease asset. It makes the information more relevant and ensures consistency.

3. To make the financial statement data and information provided to reviewers more valuable for decision-making, GASB 87 mandates the notes on such statements provide details regarding the date, relevance, and objective of a government's leasing contracts. It caters to the three accounting treatments discussed.

According to GASB 87, a lease is classified as an agreement demonstrating control of the right-to-use of another entity's non-financial asset (the intrinsic asset), as stipulated in the agreement for a time frame in exchange for payment.

This definition applies to all types of leases, including operating leases, finance leases, and operating leases with options.

The lease description needs to be broken down even more before it can be used to determine what the new standard considers a lease.

The term "control" is defined by GASB 87 as the right to access the current service capacity as well as the authority to select the form and mode of use.

The range of leased assets consists of non-financial assets under GASB 87. It includes things like property, buildings, machinery, and vehicles.

Certain asset-based leasing agreements that do not pertain to financial assets are not included in the scope of this standard. These include:

The recognition of all short-term leases with a max irrevocable term of twelve months or less can be omitted from the statement of financial position.

This is the case irrespective of whether or not the lessee exercises all the irrevocable terms.

When determining which contracts are to be deemed as leases, it is necessary to consider these definitions.

The classification of leases, which was once an essential factor in deciding whether or not an asset should be recognized in financial statements, is the primary area in which GASB 87 differs significantly from previous GASB guidelines.

Since GASB 87 only allows for the use of a single model framework, the distinctions between operating leases and capital leases have been eliminated.

According to GASB 87, every transaction that satisfies the criteria for being considered a lease must now be categorized as a finance lease.

Following the present GASB standard, the classification and accounting treatment of a capital lease are quite similar to that of a finance lease; the only difference is using different terminology.

As a direct result of this change, a large proportion of lease obligations will now be recognized both as assets and liabilities on the financial position statement.

A fraction of the payments made toward the lease will go toward reducing the amount owed on the lease, while the other portion will be recorded as interest expenditure on the statement of activities.

A comparable lease asset will also be reported in the financial position statement and amortized over the underlying asset's lease period or the useful life, whichever one is lesser.

The original proposal for GASB Statement No. 87 was submitted in 2017, and the original implementation date was set for December 15, 2019.

However, the GASB issued Statement No. 95 in May 2020, which postponed the implementation of GASB No. 87 until June 15, 2021, because of complications caused by the pandemic in governmental accounting domains.

Since then, all leases have been required to be reported as GASB 87 leases in accordance with the single model of lease accounting outlined in the GASB 87 declaration.

Having said that, the GASB recommends early adoption. Since obtaining compliance with GASB 87 can be challenging and time-consuming, it is highly recommended that consideration be given to adopting the standard as soon as possible.

The methodology proposed by the GASB is analogous to IFRS 16 in the way that the lessee will label all leases as financing agreements.

Under ASC 842, the dual lease type approach is still utilized, despite the fact that both types of leases will now be acknowledged on the balance sheet as a result of ASC 842.

There are also several other significant differences between the standards:

The COVID-19 pandemic caused numerous accounting standards, including the new ones, to have their effective dates forced back to the beginning of 2020.

These standards were formalized by both the Financial Accounting Standards Board (FASB) and the Governmental Accounting Standards Board (GASB).

ASC 842 was required to be implemented for most organizations for fiscal periods commencing after December 15, 2021, while GASB 87 was required to be established six months earlier with an effective date for accounting periods starting after June 15, 2021.

Both of these requirements are now in place and must be adhered to.

The International Financial Reporting Standard (IFRS) 16 was published in January 2016, and its requirements apply to yearly reporting periods that commenced on or after January 1, 2019.

In the absence of an implicit rate in the underlying agreement, ASC 842 permits the application of a risk-free discount rate to approximate the incremental borrowing rate.

Typically, this represents the US Treasury rate on securities with terms comparable to those of the contract. Instead of providing its own method for attributing a rate of interest for arrangements without an implicit rate, GASB 87 refers users to GASB 62 for guidance.

While the rate implied in the lease is defined by IFRS 16 as the discount rate where the aggregate of the current value of the lease payments and the unguaranteed residual value matches the total of the fair worth of the underlying asset and any upfront direct expenses of the lessor.

The first 5 years of maturities linked to leases will be reported by FASB reporters and afterward, will be reported as a single amount as well.

In contrast, GASB 87 requires the disclosure of the initial five years of payments and then does so in incremental steps of five years afterward.

Additionally, disclosure of residual value guarantees and termination penalties is not particularly required by ASC 842, but disclosure of these components is explicitly required by GASB 87.

The IFRS 16 comprises both qualitative and quantitative disclosure obligations. The financial statement users need a foundation on which to evaluate the impact that leases are having on the financial statements, and the purpose of the disclosure requirements is to provide that basis for them.

These agreements are not leases per GASB 87 and IFRS 16; hence they should be treated as financed purchases beyond the scope of the new lease guidelines.

In contrast, under ASC 842, these sorts of contracts are classified as finance leases, which is comparable to how ownership-transferring contracts were handled under the previous standard (ASC 840).

Accounting for leases is becoming increasingly sophisticated. It will become more challenging for businesses to account for leases in their financial statements accurately.

Having said that, the reform is positive because it will bring financial statements closer in line with the classifications of their assets.

Thankfully, there are professionals available to assist with this transition and several technological solutions to facilitate compliance with the new lease accounting standards. Thus, organizations must reach out to receive assistance and guidance in this transitive process.

LeasO is a cloud-based lease management software compliant to new accounting standards like GASB 87. With LeasO, you can track, manage, and centralize all your lease data in ONE place while avoiding any manual accounting error. Book a demo to know more.

.jpg)

Please submit your details and our Product Consultant will connect with you to understand your needs.

{kind=link}

{kind=link}